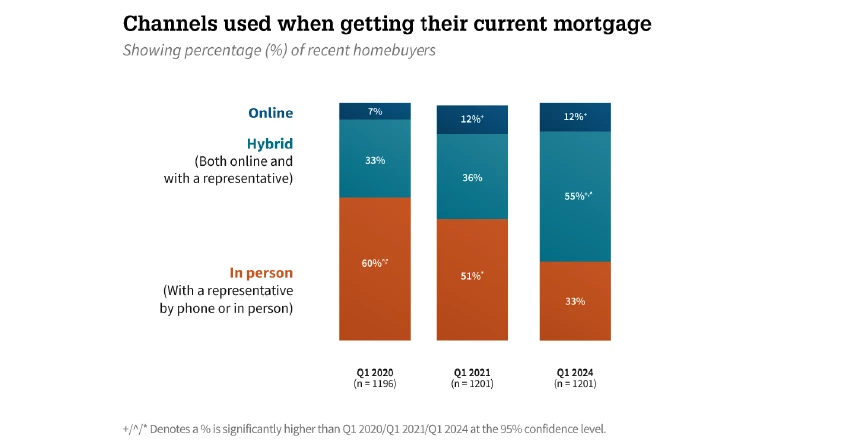

Getting a mortgage used to require manually gathering bank statements and tax documents, followed by weeks of in-person meetings and phone calls with loan officers. Today, most borrowers follow a hybrid process that combines digital tools with traditional steps—and 90% of homebuyers are interested in an even more digital mortgage experience, according to a Fannie Mae survey.

Clearly, lenders and financial services companies need to deliver faster, smoother borrower experiences that match today’s digital-first mindset. But that’s only part of the equation. Behind the scenes, lenders today often rely heavily on manual, time-consuming internal workflows. These also need to be automated for responsiveness and scalability.

To understand what this transformation involves, let’s explore what mortgage process automation is, what benefits it delivers, and which factors lenders should consider when choosing a mortgage loan automation solution.

Jump to:

What is mortgage process automation: Technologies and capabilities

How mortgage automation speeds up decision-making and reduces risk in financial services

What to look for in a mortgage processing automation solution

How AI is reshaping the mortgage industry

Why financial services leaders trust ABBYY for AI-powered mortgage automation

What is mortgage process automation: Technologies and capabilities

Mortgage process automation refers to the use of technology—including optical character recognition (OCR), natural language processing (NLP), and machine learning—to handle tasks across the mortgage lifecycle that were traditionally performed by humans.

From end to end, the mortgage process is quite intricate and complex. It involves a wide range of documents—loan applications, tax forms, bank statements, disclosures, and credit reports—all of which must be received, classified, and have their data extracted and processed. From this information, lenders must assess risks and make decisions on loan eligibility.

All of this work used to be done manually, but technology has increasingly taken over parts or even entire sections of the mortgage process. Key technologies used in mortgage processing automation include:

- Optical character recognition (OCR): This technology scans mortgage documents and turns the information into machine-readable text for efficient data extraction.

- Intelligent document processing (IDP): IDP automates the intake, classification, and extraction of data from both structured and unstructured mortgage documents.

- Artificial intelligence (AI): By identifying patterns and insights within borrower data, AI helps lenders assess risk and speed up approvals.

- Natural language processing (NLP): This branch of AI essentially gives technology systems the ability to not only read but understand and interpret human language within mortgage documents.

- Machine learning (ML): Another subset of AI, ML improves lending-related predictions over time.

What used to be a lengthy mortgage processing workflow can today be completed much faster, thanks to technology performing everything from repetitive tasks to complex calculations—then making data-driven decisions to speed up approvals.

How mortgage automation speeds up decision-making and reduces risk in financial services

Financial services companies today manage massive volumes of documents from every channel: paper mail, email, even text messages. Fidelity Financial, for example, was handling over 15,000 pages of faxed mortgage applications daily. When manual processing fell short, they turned to ABBYY intelligent automation—and started processing those thousands of pages within an hour of receipt.

Fidelity Financial’s success is just one example of how mortgage process automation helps financial services organizations stay competitive. Here are some of the key ways technology is improving how mortgages are processed:

- Efficiency and accuracy: Intelligent document processing automatically extracts clean, validated data from documents with minimal manual intervention, reducing human error.

- Regulatory compliance: Automation creates accurate audit trails for compliance with Know Your Customer (KYC), Anti-Money Laundering (AML), the Real Estate Settlement Procedures Act (RESPA), and other financial regulations.

- Cost savings: Reducing manual labor and rework can lower operational costs significantly while also freeing up staff to take on higher-value tasks.

- Crime and fraud detection: Automation can be used to help identify suspicious documents or behaviors before they can impact operations.

- Scalability: Unlike manual processes, digital workflows can easily adapt as business needs evolve. Teams can scale operations without adding overhead.

- Process visibility: Automation provides real-time insight into where documents are, where delays occur, and how work is progressing to help leaders make workflow improvements.

- Faster decision-making: By automating the flow of verified data into loan origination systems, lenders can make better decisions more quickly.

- Improved customer and employee experience: With mobile-ready and contactless solutions, customers benefit from faster application and approval experiences. In addition, employees are freed from repetitive busywork.

Beyond faster approvals and fewer manual tasks, mortgage process automation can reveal and eliminate inefficiencies that would otherwise go unnoticed. One global financial institution, for example, uncovered 550,000 hours of rework buried in its mortgage operations. By automating those processes, it reclaimed that time and reduced cycle times by more than six days. Savings on that scale represent a fundamental shift in how mortgage operations are managed altogether.